Medicare Supplement plans, which insurance companies commonly call “Medigap” plans, are optional healthcare coverage policies you can add to your existing Medicare coverage. These plans cover inpatient and outpatient services that Original Medicare Part A and B miss, giving you even more health insurance than you’d have with baseline Medicare.

There are 12 types of Wyoming Medicare Supplement plans, including two with high-priced deductibles in exchange for lower premiums, each with different monthly charges and levels of coverage.

However, the federal government standardizes all Medigap plans, so you’ll receive the same benefits with a plan regardless of where you enroll or the insurance carrier.

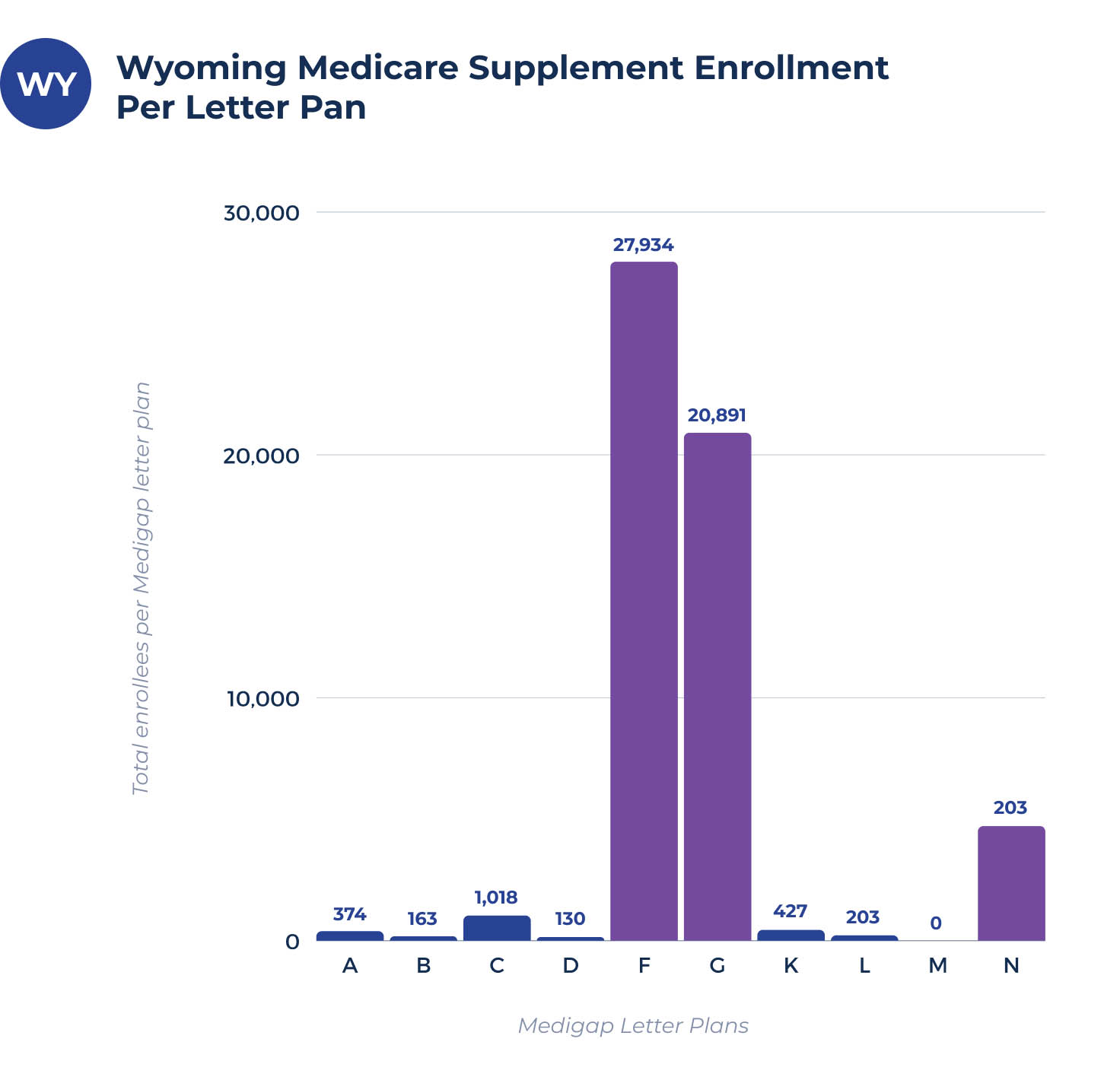

Wyoming Medicare Supplement enrollment per letter plan

In Wyoming, 51,281 people have a Medicare Supplement plan. While that overall enrollment is one of the lowest in the country, the percentage of fee-for-service Medicare enrollees participating in Medigap is one of the highest nationwide at 47%.

| PLAN | A | B | C | D | F | G | K | L | M | N |

| 438 | 208 | 1,297 | 166 | 31,332 | 11,485 | 349 | 204 | 0 | 3,747 |

What are the most common Medigap plans in Wyoming?

Plan F is the most common Wyoming Medicare Supplement option. Of the state’s 51,281 total Medigap participants, 31,332 have Plan F coverage. Medigap Plan F is also the most enrolled-in Medicare Supplement plan nationwide.

Plan G has the second-highest enrollment rate in Wyoming, with 11,485 participants, followed by Plan N with 3,747.

The only other Medicare Supplement options in Wyoming with over 1,000 enrollees are Plans C and J, with 1,297 and 1,506, respectively.

Medigap plan coverage chart for Wyoming

The benefits in Medigap plans don’t just stay the same at each Wyoming provider; they’re also constant from state to state. For example, if you’re a Plan F beneficiary in Wyoming moving out of state, you’ll find a Plan F option in your new home with the same benefits regardless of where you relocate. The only changing variable is the prices of each plan.

Medicare Supplement plans costs in Wyoming

The federal standardization that keeps Wyoming Medicare Supplement benefits are constant across providers doesn’t apply to their rates. That means your coverage will cost more or less, depending on where you enroll.

Insurance companies examine several criteria before determining your rates, including Medigap pricing method, age, gender, history of tobacco use, desired payment terms, and whether you are applying with a spouse or partner.

What’s the average cost for a Medicare Supplement plan in Wyoming?

yonming Medicare Supplement premiums can vary due to a few reasons. The monthly premium might range from $70 to $145.

Lowest premium per Medigap letter plan in Wyoming

As previously mentioned, the exact rates you pay for Wyoming Medicare Supplement plans vary based on more than age and gender. However, the average 65-year-old female Medigap enrollee can expect the following premium rates on these ten popular policies to be their most affordable options.

| PLAN | A | B | C | D | F | G | K | L | M | N |

| Premium | $96 | $130 | $137 | $115 | $118 | $101 | $54 | $67 | $104 | $73 |

Highest premium per Medigap letter plan in Wyoming

The rates in the chart below reflect the high-end premium costs for the average 70-year-old male enrollee.

| PLAN | A | B | C | D | F | G | K | L | M | N |

| Premium | $423 | $382 | $461 | $306 | $463 | $441 | $161 | $262 | $297 | $370 |

Top Medicare Supplement plan carriers in Wyoming

The chart below lists Wyoming’s five most popular Medicare Supplement providers and what they typically charge for the state’s three most enrolled-in Medigap plans.

The rates in the chart are the average monthly costs for a 65-year-old male enrollee living in Wyoming.

| CARRIERS | PLAN F | PLAN G | PLAN N |

| Nassau Life | $118 | $113 | $82 |

| American Home | $121 | $101 | $73 |

| Mountain Health | $125 | $105 | $80 |

| Lumico | $131 | $107 | $86 |

| Accendo | $132 | $118 | $79 |

Estimated Medicare Supplement plan premiums in Wyoming cities

The accompanying charts linked below provide estimated premiums for the various types of Medicare Supplement coverage for the cities listed:

FAQs

When can I apply for Medigap in Wyoming?

You can apply for Wyoming Medicare Supplement coverage anytime during your Initial Enrollment Period if you have Original Medicare Parts A and B. Your Initial Enrollment Period begins the first day of the month of your 65th birthday and lasts for the next six months.

To enroll in Medigap coverage during your Initial Enrollment Period, you must contact your insurance provider and request an application.

You can also apply for a Medigap plan during any time of year, so long as you have Medicare Parts A and B, but doing so outside of your six-month open enrollment may subject you to medical underwriting.

Can you add Medigap plans at any time in Wyoming?

Unlike Medicare Advantage plans, you can enroll in a Medigap plan anytime. However, enrolling in a Medicare Supplement plan outside your six-month Initial Enrollment Period may subject you to plan denial.

During your first six months of Medicare, you can enroll in a Medigap plan without risking a rejected application since Medigap providers are legally obligated to sell you a policy without medical underwriting during this time.

Can Medigap insurance be denied for pre-existing conditions in Wyoming?

Medigap insurance providers can and often do refuse to cover pre-existing conditions. Additionally, those that do offer pre-existing condition coverage often require you to pay out of pocket for those ailments for the first six months of your plan.

Insurance providers call that coverage lapse the “pre-existing condition waiting period.” However, you can avoid it altogether by applying for Wyoming Medicare Supplement coverage during your Initial Enrollment Period.

When can you make changes to Medigap in Wyoming?

You can change your Medigap plan to any other policy at any time during your six-month open enrollment.

However, since the federal government standardizes Medicare Supplement coverage in Wyoming, you cannot change your plan’s benefits, only the plan itself.

Can you switch from Medicare Advantage to Medigap in Wyoming?

Wyoming does allow you to switch from Medicare Advantage to Medigap, but it’s a more complex process than applying for one without the other.

First, you must drop your Medicare Advantage coverage and re-enroll in Original Medicare Parts A and B. Then, after completing both steps, you can call your insurance provider and request a Medigap plan application.

How to sign up for Medicare Supplement plans in Wyoming

Medigap.com makes it easy for you to find affordable Wyoming Medicare Supplement coverage. Our team works with all insurance providers and compares rates from their Medigap plans for free so that you can find your best fit within minutes.

We know how frustrating and confusing the Medicare plan enrollment process can be. Instead of spending hours navigating various plan options and hundreds of potential benefits, let the Medigap.com team help you find the best plan for your health needs and budget.

Call our team or complete our online rate form to get rates today.