The Medicare Annual Enrollment Period is an essential window of opportunity. Medicare beneficiaries can take advantage of this enrollment window each year in the fall.

For beneficiaries currently enrolled in either a Medicare Advantage or Part D drug plan, you’ll be able to make necessary changes to get the benefits you need at the costs you can afford.

We’re about to break it down to help you understand why this annual enrollment window is so important.

How the Medicare Annual Enrollment Period Works

It’s easy to confuse the Medicare Annual Enrollment Period with the open enrollment periods. They do have some things in common. But their dates are entirely different and vary in the changes you’re allowed to make to your health care plan.

Here’s what you can expect from the Annual Enrollment Period:

- You can switch from Original Medicare to Medicare Advantage or from Medicare Advantage back to Original Medicare

- You can enroll in, change, or cancel your current Medicare Part D prescription drug plan

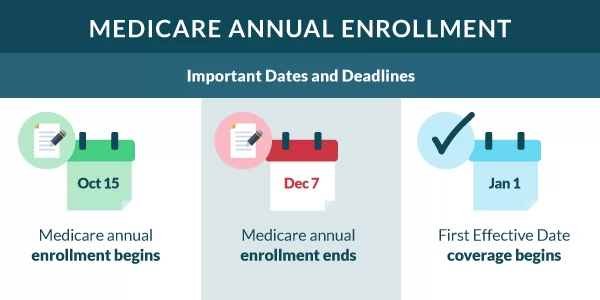

Medicare beneficiaries can take advantage of the Medicare Annual Enrollment Period between October 15 and December 7th each year. Both Medicare Advantage & Part D plans are guaranteed to change each year.

It’s crucial to stay on top of what your plan offers and its total costs. Your new plan will go into effect on January 1 of the following year.

The Open Enrollment Period is a little more complex. There are two different types of OEPs:

- The Medicare Advantage Open Enrollment Period – You can make changes to your Medicare Advantage plan during the Medicare Advantage OEP if and only if you’re currently enrolled in a Medicare Advantage plan.

- Medicare Supplement Open Enrollment Period – If you have Original Medicare, you can shop between different Medigap plans and have your whole six-month Open Enrollment Period to settle on a plan. Another benefit of enrolling during this window is that you can’t be denied coverage. There’s no need to prove you’re in good health to be given coverage at a fair premium.

Here’s What You Can Do During the Annual Enrollment Period

Are you interested in trying out Medicare Advantage for the first time? Do you miss your Original Medicare and want to switch back?

What about your prescription drug plan? Does your formulary cover all the prescriptions you need at a reasonable price? If you’ve been contemplating these questions lately, you want to take advantage of the AEP.

Switching Between Original Medicare and Medicare Advantage

If you have a Medicare Advantage plan and want to return to your Original Medicare, you can do that during the AEP.

Likewise, if you have Original Medicare but want to switch to Medicare Advantage, you can also do that during this window of opportunity. If you switch to Original Medicare, you can enroll in a Medicare Supplement plan anytime.

Change Your Prescription Drug Plan

Your drug plan’s formulary (the drugs you can purchase at a subsidized discount) and the prices you pay are likely to change annually.

If you have Original Medicare and notice inconvenient changes to your Medicare Part D prescription drug plan, you can shop around and choose a different plan. You can do the same if you have Medicare Advantage and a separate prescription drug plan.

You can also enroll in Medicare Part D if switching from Medicare Advantage to Original Medicare. Likewise, you can cancel your Part D prescription drug coverage entirely.

Here’s Why You Should Review Your Healthcare Coverage Before Each Annual Enrollment Period

We touched on it a little bit so far, but the reality is that your healthcare plan will change annually. Sometimes it’s simply a modest premium increase.

Sometimes your prescription drug program formulary may not cover the life-saving drugs you need anymore. You might even lose access to the doctors and health care providers you need most.

Changes in Medical Costs

Regardless of your Medicare plan type, your premiums will likely increase yearly. This premium is tied to the cost of medical care for the average beneficiary and inflation rates.

Premium increases occur for Medicare Advantage, Medicare Supplement, and Medicare Parts A and B. For your private plans like Medicare Advantage, you may also have changes in your coinsurance and copayment costs.

Changes in Medication and Provider Access

Private drug plans can change their formulary every year. The formulary provides a list of covered drugs and outlines the cost you’ll pay for those prescriptions.

If you have Medicare Advantage, certain doctors and facilities may leave or be eliminated from your provider network.

Conversely, if you have Original Medicare, providers and facilities may choose not to accept Medicare assignment, forcing you to either find care elsewhere or pay out-of-pocket.

Benefits, Ratings, and Travel

Your benefits could change or become more expensive from one year to the next. Benefit reductions are more common with private insurance plans, but those plans can never offer you less than the benefits of Original Medicare without violating the law.

Furthermore, if your plan receives a low rating from its customers, you may no longer feel confident paying for such a plan.

Lastly, how often you travel will significantly affect what sort of plan you want. If you’re a snowbird or travel frequently, you probably aren’t want to purchase an HMO plan with a medical network limited to a small zip code.

PPO plans are better for travelers or Original Medicare since providers all over the country accept Medicare assignment.

Medicare Annual Enrollment Period Eligibility

You must be enrolled in Original Medicare (Parts A and B) before taking advantage of the AEP. Beneficiaries may not be enrolled if they have other qualifying coverage, such as an employer health plan.

If that’s the case, you’ll have to wait for either a Special Enrollment Period or the General Enrollment Period to enroll in Original Medicare.

FAQs

What is the Annual Coordinated Enrollment Period?

It’s common for the AEP to go by many different names, like how Medicare Part C and Medicare Advantage are the same.

The Annual Coordinated Enrollment Period is just another saying “Annual Enrollment Period” and “Annual Election Period.”

People may also refer to the AEP as the “Fall Open Enrollment Period,” but in reality, open enrollment periods are separate things that follow different rules.

When does the Medicare Annual Enrollment Period start and end?

It starts on October 15 and ends on December 7 every year like clockwork. If you change your health plan, your new plan and benefits will go live on January 1.

What if I want to switch from Medicare Advantage to Original Medicare and purchase a Medicare Supplement?

You can enroll in a Medicare Supplement at any point in the year. Unlike Original Medicare, Medigap plans don’t come with an annual enrollment window.

If you choose to take advantage of the AEP and switch back to Original Medicare, you can enroll in a Medigap plan at that time.

However, you’ll have to undergo medical underwriting if you’re outside your one-time Medigap Open Enrollment Period. The only exception is if you qualify for a Special Enrollment Period.

Do I have to worry about changes to my Medicare Supplement plan during the Medicare Annual Enrollment Period?

Medicare Supplement plans are standardized, so your benefits will never change. You may, however, see a rise in your monthly premium. If the increase is too drastic, you can switch plans at any time of the year. You don’t have to wait until the AEP to do so.

How do I change my healthcare coverage during the Annual Enrollment Period?

You can try and do it alone. You can call a trusted local insurance agent to help you out. Or you could ask one of our talented and capable agents to review your information and guide you toward the right decision. We’re standing by and ready to hear from you, so don’t hesitate to reach out and contact us.